Self-Employed Mortgage Checklist for Ontario Buyers

Self-Employed Mortgage Checklist for Ontario Buyers

Buying a home in Ontario is already a major milestone, but for self-employed buyers—entrepreneurs, freelancers, contractors, and small business owners—the path to mortgage approval can feel like navigating a maze. Unlike salaried employees, who can hand over a T4 slip and recent pay stubs, self-employed individuals must prove their income stability and financial strength in more complex ways.

If you’re self-employed and planning to buy a home in Ontario, this comprehensive checklist will help you understand what lenders expect, what documents you’ll need, and how to prepare so you can approach the process with confidence.

Why Is It Harder for Self-Employed Buyers to Get a Mortgage?

Self-employed buyers don’t have guaranteed paycheques. Their income can fluctuate seasonally, vary month to month, and often includes business write-offs that reduce taxable income on paper. While this is good for lowering taxes, it can make your income look smaller in the eyes of lenders.

Lenders want reassurance that you can handle mortgage payments consistently, even during slower months. This is why they often require more documentation and conduct deeper reviews for self-employed applicants.

The Self-Employed Mortgage Checklist (Ontario Edition)

Here’s the step-by-step checklist of what you’ll typically need when applying for a mortgage as a self-employed buyer in Ontario:

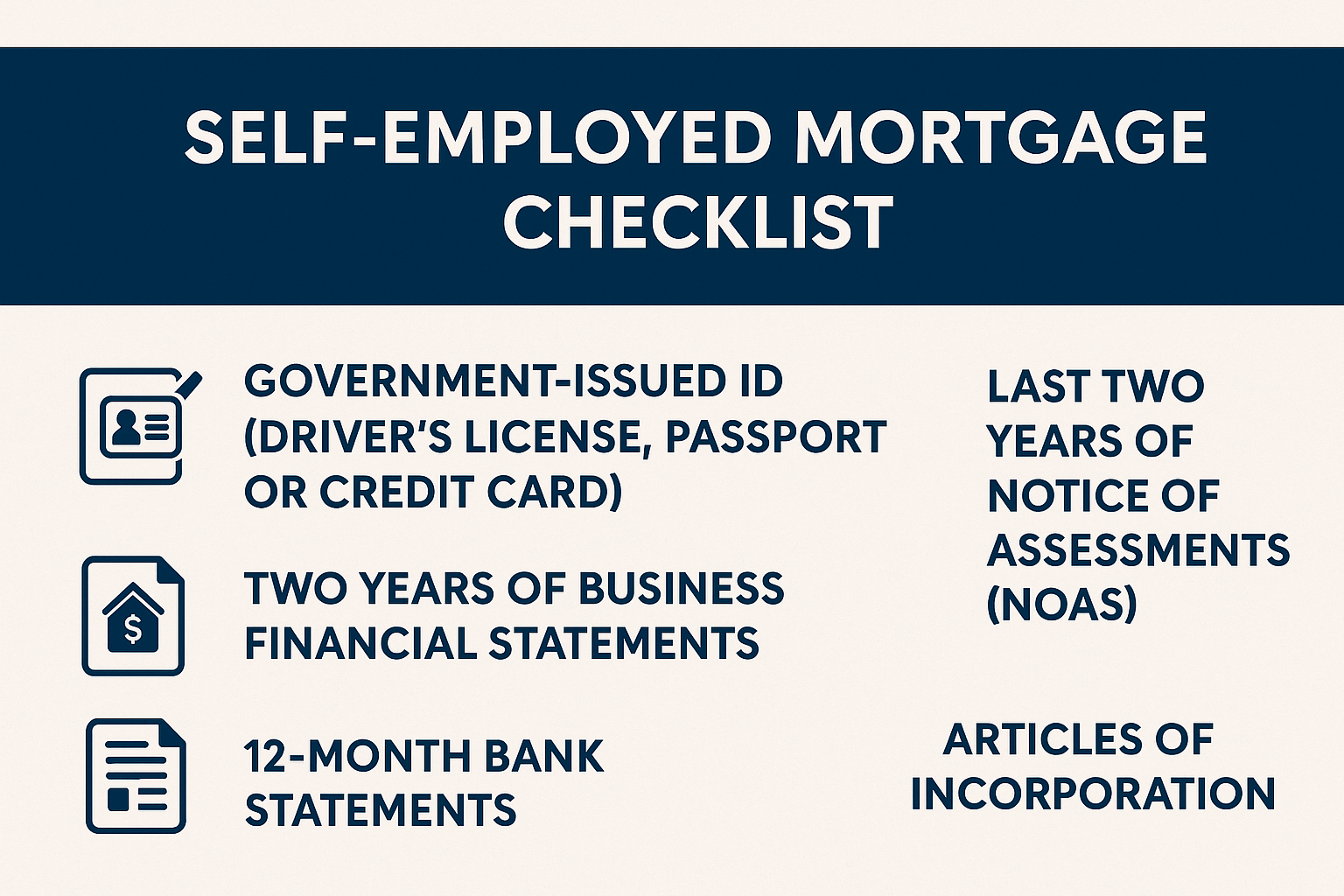

✅ 1. Proof of Identification

You’ll need at least two pieces of government-issued ID. Common options include:

- Driver’s license (must be valid and not expired)

- Passport

- Permanent resident card

- Secondary ID (credit card with your name, SIN card, or other acceptable forms as required by the lender)

✅ 2. Proof of Business Ownership

Lenders want to confirm that you are actively running a legitimate business. Documents that may be requested:

- Articles of Incorporation (if you own a corporation)

- Master Business License (if you’re a sole proprietor or partnership)

- GST/HST registration

- Business contracts or invoices showing ongoing work

✅ 3. Proof of Income (Tax Documentation)

Unlike employees who provide pay stubs, self-employed individuals need at least two years of tax records. These typically include:

- T1 General Tax Returns (full copies, not just the summary)

- Notice of Assessment (NOA) for the last two years

- Business financial statements (if incorporated)

- In some cases, lenders may also ask for bank statements showing deposits

✅ 4. Proof of Down Payment

Every buyer must show where their down payment is coming from. For self-employed buyers, lenders may ask for a clearer paper trail:

- 90-day history of bank accounts (to prove funds are not borrowed)

- Gift letter (if family is helping with down payment)

- Investment statements (RRSP, TFSA, mutual funds, etc.) if funds are withdrawn from savings

✅ 5. Credit Report

Your credit score plays a huge role in approval. In Ontario, most A-lenders prefer scores of 680+. You should:

- Review your credit report before applying (through Equifax or TransUnion)

- Pay down revolving debts like credit cards or lines of credit

- Avoid late payments, as they can hurt your approval chances

✅ 6. Debt & Expense Documentation

Lenders calculate your GDS (Gross Debt Service) and TDS (Total Debt Service) ratios to see if you qualify. They’ll want to see:

- Loan statements (car loans, personal loans, lines of credit)

- Credit card balances

- Business debts (if personally guaranteed)

- Lease obligations

✅ 7. Business Stability Proof

If you’ve been self-employed for less than two years, you may face additional scrutiny. Lenders may want:

- Client contracts or invoices that show steady income

- Proof of long-term clients

- A letter from your accountant confirming your business operations

Ontario-Specific Mortgage Considerations

1. Stress Test Rules

All buyers in Ontario must pass the mortgage stress test, qualifying at the greater of 5.25% or 2% above the offered rate. This means your income documentation must show that you can afford payments at a much higher rate than your actual mortgage.

2. Minimum Down Payment

- Homes under $500,000 → 5% minimum down payment

- Homes $500,000 to $999,999 → 5% on the first $500,000 + 10% on the remainder

- Homes $1,000,000 to $1,499,999 → 10% minimum down payment

- Homes $1,500,000+ → 20% minimum down payment (not CMHC-insurable)

3. CMHC Default Insurance

If your down payment is less than 20% and your home price is below $1,000,000, you’ll need mortgage default insurance (through CMHC, Sagen, or Canada Guaranty). For self-employed borrowers, insurers also require proof of income and may apply stricter guidelines.

Strategies to Improve Approval Chances as a Self-Employed Buyer

- Keep Personal and Business Finances Separate

Maintain clear boundaries between business and personal accounts. This simplifies proof of income. - Avoid Excessive Write-Offs

While tax deductions lower taxable income, they also reduce the income lenders recognize. Balance tax savings with mortgage qualification needs. - Work With a Mortgage Broker

Mortgage brokers have access to alternative lenders (B-lenders and private lenders) if you don’t meet A-lender requirements. - Build a Strong Credit Profile

Pay bills on time, keep credit utilization under 30%, and avoid applying for too much new credit before mortgage shopping. - Save a Larger Down Payment

The higher your down payment, the less risky you appear to lenders. A 20%+ down payment also helps avoid CMHC premiums.

Alternative Mortgage Options for Self-Employed Ontarians

If traditional lenders don’t approve you, there are still options:

- B-Lenders: More flexible, but rates and fees may be slightly higher.

- Private Lenders: Best for buyers with unique situations or credit challenges. These are usually short-term solutions.

- Stated Income Programs: Some lenders allow self-employed applicants to state income, supported by reasonability tests and bank statements.

Common Mistakes Self-Employed Buyers Should Avoid

- Waiting until the last minute to prepare documents

- Writing off too much income in taxes before mortgage application

- Not checking credit score early

- Mixing personal and business finances

- Assuming you can’t qualify—many self-employed Ontarians get approved with the right guidance

Final Thoughts

Being self-employed shouldn’t stop you from becoming a homeowner in Ontario. The key is preparation. By gathering the right documents, maintaining strong credit, and working with a mortgage professional who understands self-employed income, you can confidently approach lenders and secure the mortgage you need.

Remember, every situation is unique. A mortgage broker can help match you with lenders that understand your business model and financial history. Whether you’re a contractor in Vaughan, a freelancer in Barrie, or a small business owner in Oshawa, the dream of homeownership in Ontario is absolutely within reach

Call/Text Garry Now

437-961-0004