Buying vs Renting: What 30 Years Later Really Looks Like

Buying vs Renting: What Happens Over 30 Years?

Let’s look at two people: Sarah and Mike.

They both start at age 30 with similar jobs, similar income, and the same goal — to live comfortably in Ontario. But they make two different choices. Sarah buys a home. Mike decides to rent.

Sarah’s 30-Year Homeownership Journey

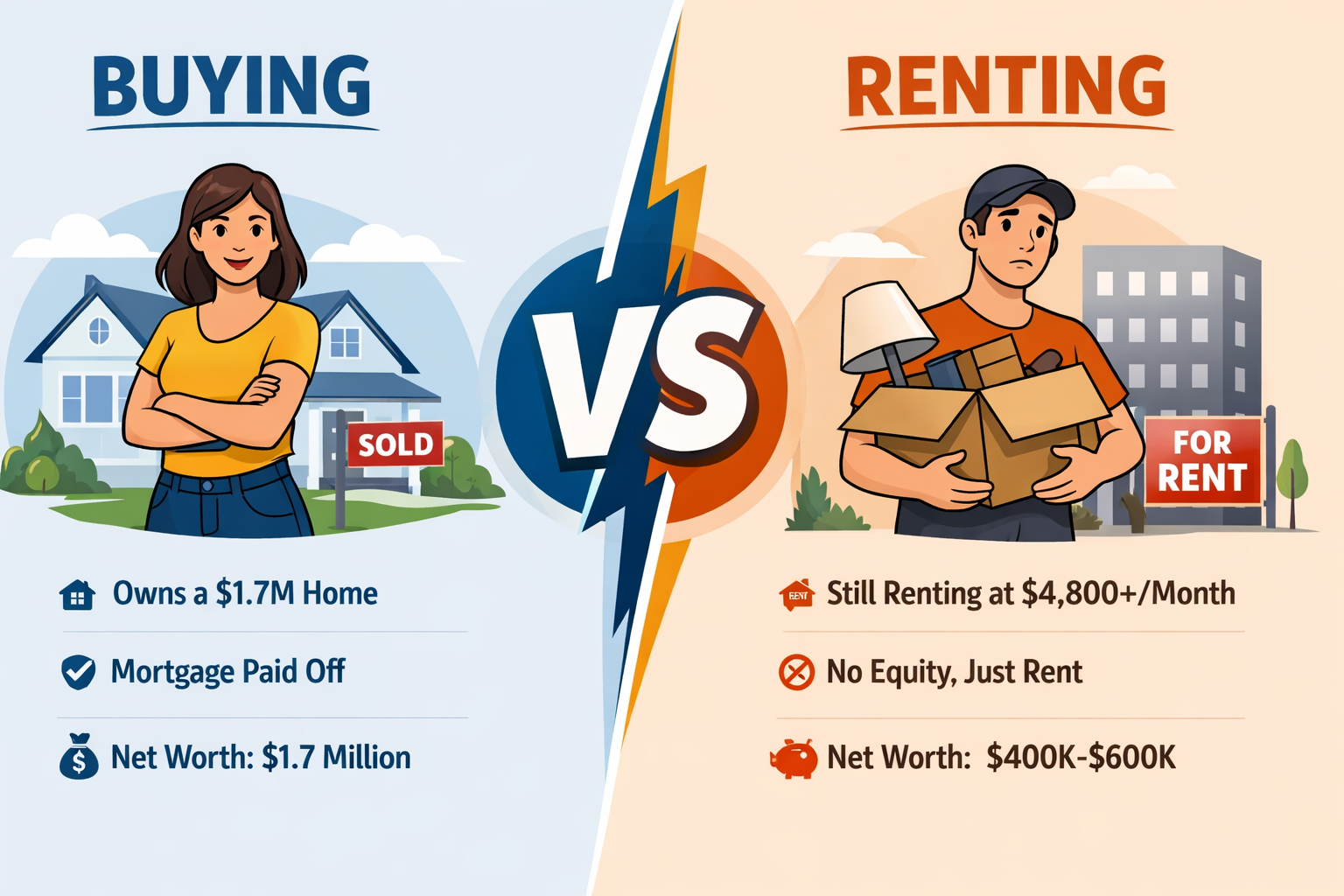

In 2024, Sarah buys her first home — a $700,000 property. She puts down 20% and gets a 30-year mortgage at a fixed 5% rate. Her monthly payment, including property taxes and maintenance, is around $3,000.

Sarah commits to her plan. She pays her mortgage every month. Over time, she builds equity, and her home grows in value. By year 30:

- Her mortgage is fully paid off.

- She owns a home that’s now worth about $1.7 million, assuming just 3% growth per year.

- She’s mortgage-free. Her monthly housing cost drops to just maintenance and property taxes — maybe $500–$700 a month.

- She never had to move unless she chose to. She enjoyed stability, ownership, and control over her home.

Mike’s 30-Year Renting Journey

Mike decides that homeownership is too expensive or too risky. He rents instead. In 2024, his rent is $2,500 per month — less than Sarah’s mortgage payment. He figures he’ll invest the difference.

But over time, rent rises. At 2.5% annual rent increases (which is normal), his rent in year 30 is over $4,800 per month.

Mike never builds equity. He pays over $1.3 million in rent across 30 years. Even if he saves and invests a little each year, he ends up with around $400,000–$600,000 saved — much less than the $1.7 million home equity Sarah has.

He still has to pay rent forever, even in retirement. And he may have moved several times due to landlord changes, increasing rents, or limited rental options.

So Who Comes Out Ahead?

After 30 years:

- Sarah owns a home free and clear, worth around $1.7 million. Her living costs are low, and she has full control of her property.

- Mike has no real estate assets, spent more than $1.3 million on rent, and will likely continue renting — with rising costs — into retirement.

Even if Mike saved a portion of his rent difference, it doesn’t match the value and security Sarah now has.

The Verdict

Buying wins. Not just in wealth, but in long-term stability.

If you’re on the fence, remember: real estate is a long game. It’s not about timing the market — it’s about time in the market.

Ready to Explore Your Buying Options?

You don’t need to have it all figured out. That’s what I’m here for.

Let’s talk about what’s possible for you today. Whether you’re ready now or just planning ahead, we can build a strategy to get you into your first home and start your wealth journey.

👉 Contact me here and let’s talk next steps.