Brampton Is in Serious Trouble: Mortgage Delinquencies Are Rising Fast

Brampton Homeowners Are Getting Crushed — And Mortgage Delinquencies Prove It

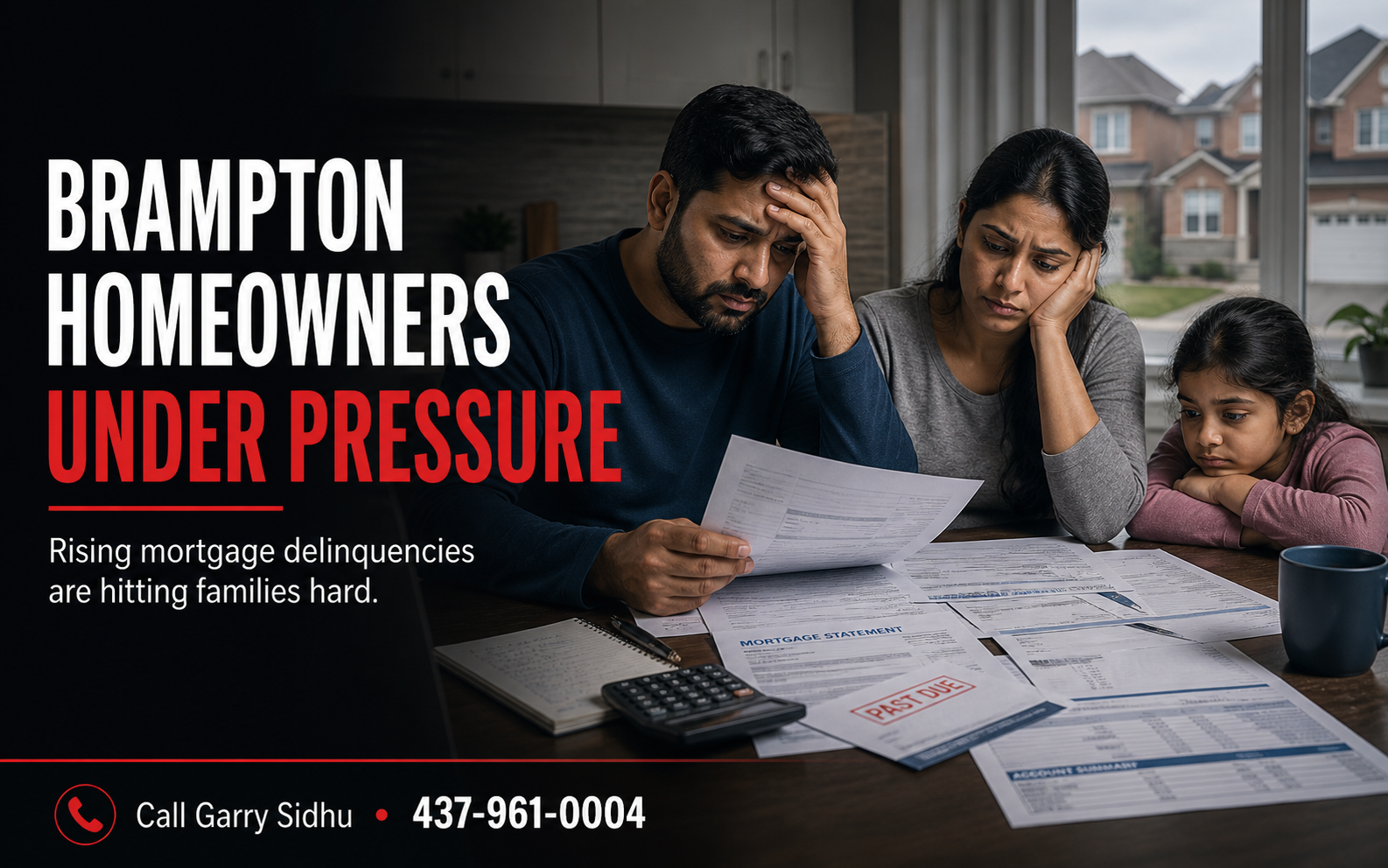

Brampton is not just “feeling pressure.”

Brampton is getting hit hard.

And the mortgage delinquency numbers are now showing what many homeowners have been quietly feeling for months.

According to recent reporting based on Equifax Canada data, Brampton is being reported as the Ontario city leading Canada’s surge in mortgage delinquencies. The reported mortgage delinquency rate reached 0.6% in Q4 2025, compared with about 0.26% nationally.

That may sound like a small number.

It is not.

When mortgage delinquencies more than double the national average, that is not normal.

That is a warning sign.

It means more homeowners are falling behind. It means more families are under pressure. It means the financial stress that used to be hidden is now starting to show up in the data.

And if you own a home in Brampton, Mississauga, Vaughan, Toronto, Pickering, Oshawa, Barrie, Bradford, or anywhere in Ontario, this should get your attention.

Because Brampton may be the headline today.

But the same pressure is sitting inside thousands of homes across Ontario.

Brampton Became the Perfect Storm

Let’s be honest.

Brampton was one of the cities where people stretched hard during the real estate boom.

Prices went crazy.

Bidding wars were everywhere.

Families were buying homes at high prices because they thought if they did not buy then, they would never get in.

A lot of people bought when rates were low.

A lot of people took on big mortgages.

A lot of people added credit card debt, car loans, lines of credit, and family obligations on top.

Now the market is different.

Rates are higher.

Renewals are coming.

Expenses are up.

Income has not kept up.

And the breathing room is gone.

That is why Brampton is becoming Canada’s mortgage stress warning sign.

Not because everyone is irresponsible.

Not because people do not work hard.

But because the numbers stopped working for a lot of households.

The Real Problem Is Not Just the Mortgage

Most homeowners do not fall behind because of one thing.

It is usually a pile-up.

The mortgage is high.

The car payment is high.

Credit cards are carrying balances.

Property taxes went up.

Insurance went up.

Groceries went up.

Daycare costs are brutal.

Fuel, utilities, repairs, and everyday life became more expensive.

Then the mortgage renewal comes in higher.

That is when things start breaking.

A family that was already tight suddenly has to absorb another few hundred or even a thousand dollars per month.

For many people, that money does not exist.

So they borrow.

Then they borrow again.

Then they start juggling payments.

Then one payment gets missed.

Then another.

That is how mortgage delinquency starts.

Quietly.

Slowly.

Then all at once.

Renewal Shock Is the Real Monster

A lot of homeowners are not in trouble because of the mortgage they have today.

They are in trouble because of the mortgage they are about to renew into.

If someone bought or refinanced during the low-rate period, their current payment may not reflect today’s reality.

When that mortgage renews, the payment can jump hard.

And for homeowners already carrying debt, that increase can be the final punch.

This is why renewal planning is not optional anymore.

If your mortgage is renewing in the next 6 to 18 months, you should not be sitting around waiting for your bank to send you a letter.

That is not a plan.

That is a reaction.

And reacting late is expensive.

The Bank’s Renewal Letter Is Not Your Strategy

Many homeowners make the same mistake.

They wait until their lender sends them a renewal offer.

Then they accept whatever is in front of them because they are busy, stressed, or scared to look deeper.

That can cost thousands.

Your bank’s renewal offer is just one option.

It may not be the best rate.

It may not be the best structure.

It may not help with your debt.

It may not solve your cash flow problem.

And if your financial situation has changed, you may need a completely different strategy.

You may need to look at refinancing.

You may need debt consolidation.

You may need a B-lender option.

You may need a second mortgage.

You may need a private mortgage bridge.

You may need to restructure before your credit gets damaged.

But the key is timing.

The earlier you review your file, the more options you usually have.

The later you wait, the more expensive the options usually become.

Waiting Until You Miss a Payment Is a Bad Move

This needs to be said clearly.

Do not wait until you miss a mortgage payment.

Once you miss payments, everything gets harder.

Your credit score can drop.

Your lender may become less flexible.

Your refinance options may shrink.

Your file may move from clean to urgent.

And urgent mortgage files are rarely cheap.

If you are already feeling pressure, that is the signal.

Not the missed payment.

Not the collection call.

Not the power of sale notice.

The pressure is the signal.

If your mortgage, debts, and monthly bills are already making you uncomfortable, you need to review your options now.

What Brampton Homeowners Should Review Right Now

If you own a home in Brampton, this is the checklist:

Your mortgage renewal date.

Your current interest rate.

Your current mortgage balance.

Your monthly payment.

Your property taxes.

Your credit card balances.

Your line of credit balances.

Your car loans.

Your total monthly debt payments.

Your credit score.

Your current home value.

Your available equity.

Your income stability.

Your backup plan if your bank says no.

Most people do not know these numbers clearly.

That is the problem.

You cannot fix what you refuse to look at.

Debt Consolidation Could Help Some Homeowners Breathe Again

For some Ontario homeowners, the mortgage payment is not the only issue.

The real pressure is coming from high-interest debt.

Credit cards.

Lines of credit.

Personal loans.

Car payments.

Tax debt.

Business debt.

When all of those payments stack up, the household cash flow gets destroyed.

A mortgage refinance or home equity solution may help consolidate some of that debt into one lower monthly payment.

But this has to be done carefully.

The goal is not to “free up money” so you can start spending again.

The goal is to reduce pressure, protect the house, and create a real plan.

Debt consolidation only works when it comes with discipline.

Otherwise, you are just moving the problem around.

This Is Not About Panic. It Is About Reality.

Some people will see the Brampton mortgage delinquency headline and say the market is crashing.

That is too simple.

The smarter view is this:

Brampton is showing us where the pressure is breaking first.

High prices.

Big mortgages.

Heavy household debt.

Higher renewal rates.

Less affordability.

Less breathing room.

That combination is dangerous.

It does not mean every homeowner is doomed.

But it does mean ignoring the problem is foolish.

The market has changed.

Homeowners need to change their strategy with it.

What This Means for Buyers

For buyers, this market may create opportunity.

Not because homeowners are struggling.

Nobody should celebrate that.

But when mortgage pressure rises, the market often becomes less emotional.

Sellers may become more realistic.

Conditions may come back.

Negotiation may improve.

Bidding wars may slow down.

Buyers may finally have room to think.

That is good for prepared buyers.

But you still need a strong pre-approval.

Not a fake online estimate.

Not a soft conversation.

A real mortgage review.

Because in this market, the best buyers are the ones who know exactly what they can afford before they make an offer.

What This Means for Sellers

For sellers, the message is direct.

Do not overprice your home and hope.

That strategy worked in 2021.

It does not work the same way today.

Buyers are more careful.

Banks are more careful.

Appraisals matter.

Affordability matters.

Monthly payments matter.

If you need to sell because your mortgage is renewing, your debt is too high, or your cash flow is getting tight, you need to be realistic early.

You may have more options than selling.

But you need to review them before you are forced into a corner.

What This Means for Ontario Homeowners

Brampton is the warning sign.

But this is bigger than Brampton.

Homeowners across Ontario are dealing with the same pressure.

People in Vaughan, Mississauga, Toronto, Pickering, Oshawa, Barrie, Bradford, Newmarket, and the GTA are all facing the same basic problem:

The cost of owning a home has changed.

The mortgage market has changed.

The renewal environment has changed.

And pretending everything is fine will not fix anything.

If your mortgage is renewing soon, you need to know your numbers.

If your debt is getting uncomfortable, you need to know your options.

If your payments are starting to feel heavy, you need to act before the situation gets worse.

The Bottom Line

Brampton homeowners are getting crushed because the math has changed.

The boom-time mortgage, the higher-rate renewal, the expensive debt, and the rising cost of life are all hitting at the same time.

That is why mortgage delinquencies are rising.

That is why this headline matters.

And that is why homeowners should not wait until they are behind to ask for help.

Once you miss payments, the game changes.

Your options become fewer.

Your costs can go higher.

Your stress gets worse.

The smart move is to review your mortgage before the problem becomes urgent.

Need Help Before Your Mortgage Gets Worse?

If you are in Brampton, Vaughan, Bradford, Barrie, Pickering, Oshawa, Toronto, Mississauga, or anywhere in Ontario, now is the time to review your mortgage.

Whether you are dealing with a renewal, rising payments, credit card debt, line of credit debt, missed payments, or simply want to know your options before things get worse, I can help you look at the numbers.

Do not wait until the bank says no.

Do not wait until you miss a payment.

Do not wait until your options become expensive.

Call Garry Sidhu today at 437-961-0004 to review your mortgage options before the pressure gets worse.

You may have more options than you think.

But you need to look early.